It’s estimated that the world must invest trillions of dollars to tackle climate change by 2050. We look at the opportunities this could bring.

“It’s now or never, if we want to limit global warming to 1.5C. Without immediate and deep emissions reductions across all sectors, it will be impossible.”

These are the words of Professor Jim Skea,1 co-chair of the Intergovernmental Panel on Climate Change (IPCC), upon the release of its Climate Change 2022: Mitigation of Climate Change report. Here, we take a look at the IPCC’s key findings and discuss the implications for investors.

A sizable task

The IPCC report outlines the world’s climate-mitigation progress so far. This includes the pathways required to meet the goals of the Paris Agreement, as well as the role different sectors can play to get us there. The findings are clear: to avoid catastrophic climate change, greenhouse gas (GHG) emissions must peak before 2025 and then nearly halve (43%) from 2019 levels by 2030.2

Yet, today’s trajectory is simply not compatible with that message. GHG emissions - which have risen by more than 54% since 1990 - are now at their highest levels in human history. Scientific consensus projects warming in the region of 3C, even if countries achieve their Nationally Determined Contributions.3 The case for immediate and deep emissions reductions is painfully clear. The cost of no climate action far outweighs the cost of taking action.

Reasons for optimism

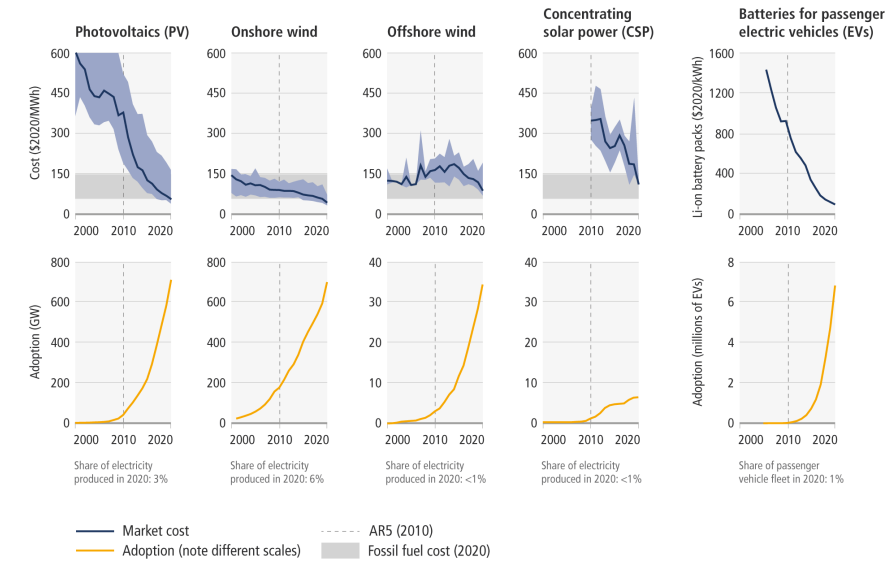

Decarbonization efforts are already underway and we've seen several promising trends. Companies have built capacity in several climate-related sectors. This has driven competition, technology improvements and economies of scale. As a result, costs for key technologies such as wind and solar have fallen by as much as 85% over the last decade4 - far further and faster than initially expected.

Decarbonization efforts are already underway and we’ve seen several promising trends.

Figure 1: The unit costs of some forms of renewable energy and of batteries for passenger EVs have fallen, and their use continues to rise.

Source: IPCC, 2022: Summary for Policymakers. In: Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change [P.R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, J. Malley, (eds.)]. Cambridge University Press, Cambridge, UK and New York, NY, USA.

Despite this, some critics have described climate change as the greatest market failure of all time. Thankfully, policymakers are starting to act. Many are internalizing the cost of emitting. Instruments such as the European Union’s Emissions Trading Scheme (ETS) are beginning to show their worth. China, the world’s largest GHG emitter, now has its own ETS to price carbon.

Governments are also gaining greater understanding of the energy transition’s broader benefits. The UK and German governments recently published their energy security strategies, which leaned heavily on renewable energy to reduce dependence on Russian oil and gas.

But this is not enough. The IPCC is clear the world must do three things:

- Double down on current mitigation efforts

- Accelerate the next wave of decarbonization

- Do so immediately

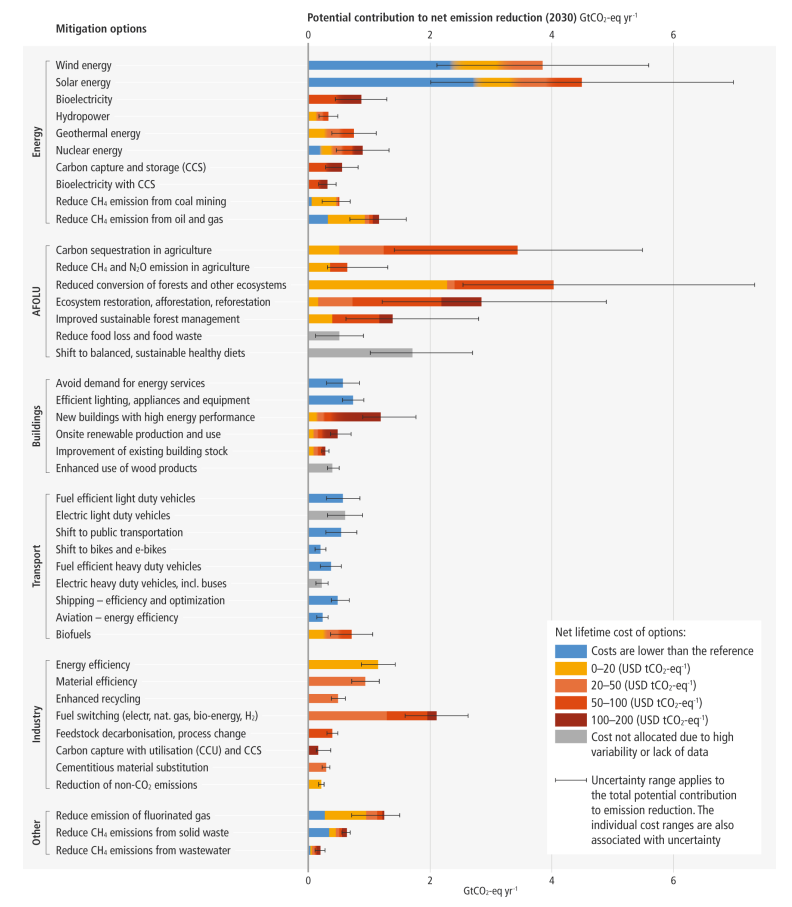

The figure below breaks this down into the key sectors and mitigation solutions. Unsurprisingly, energy, transport, industry, buildings and land use all feature prominently. Increasing energy efficiency across the economy is also vital. The IPCC shows that reducing energy demand could cut global emissions by as much as 70% by 2050.5 And, although previously an implicit requirement, the IPCC has now explicitly highlighted carbon removal methods such as Direct Air Capture as necessary to counteract residual emissions and reverse any emissions overshoot.

Figure 2: Overview of mitigation options and their estimated ranges of costs and potentials in 2030

Many options available in all sectors are estimated to offer substantial potential to reduce net emissions by 2030. Relative potentials and costs will vary across countries and in the longer term compared to 2030.

Source: IPCC, 2022: Summary for Policymakers. In: Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change [P.R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, J. Malley, (eds.)]. Cambridge University Press, Cambridge, UK and New York, NY, USA.

Significant investment opportunities

To achieve this, the IPCC estimates the world must invest nearly $130 trillion in decarbonization before 2050.6 This is a huge opportunity for companies providing energy transition solutions. It is also a significant opportunity for investors who can identify and back businesses that deliver high impact and financial returns.

These factors have manifested themselves in the performance numbers of companies aligned with the energy transition. Over the past five years7 the MSCI’s World Climate Paris Aligned index outperformed the MSCI ACWI Index by 24 percentage points; the S&P Global Clean Energy Index outperformed by 92 percentage points over the same period.8That said, since the COP26 Glasgow summit ended on November 12, 2021, those same indexes have materially underperformed the MSCI ACWI. For the period from November 12, 2021 through May 11, 2022, the MSCI ACWI retuned -18.1%, compared to -20.4% for the MSCI World Climate Paris Aligned Index and -31.7% for the S&P Global Clean Energy Index.9 However, the broad market sell-off for climate solutions has not been equal. So, there are clearly risks as well as opportunity across companies.

What does this mean for investors?

First, let’s address the recent market slump. The Covid-19 pandemic has upended the supportive macroeconomics of the last decade. Supply chains have been materially disrupted. Central banks from the US to Australia are hiking interest rates to tackle rapidly rising inflation.

Companies that are unable to manage cost increases and supply delays are feeling the pinch. Early-stage growth companies have also been hit, as investors look for defensive stocks with lower valuations. Climate-focused companies can often fit into either of these categories. Against this backdrop, we believe active investors are best placed to identify the most resilient and promising solutions providers.

Further, the current rotation provides opportunities where markets have unfairly discounted the long-term quality and fundamentals of individual companies. Equally, there are risks where markets have attached overly demanding expectations to some companies. In-depth research and direct company engagement can help investors sift through the noise.

Lastly, investors should also consider that, while the world urgently needs to accelerate climate action, a "disorderly" transition would create its own risks. For example, the necessary materials and infrastructure to achieve net zero are not yet fully in place. Companies also need to fundamentally reconfigure their supply chains. These factors are creating headwinds. But we must remember, this is a transition — not an overnight switch.

Final thoughts…

Climate action is a $130 trillion opportunity. The recent market sell-off also means several climate-focused firms are trading at a discount. These forward-looking businesses have the potential to help facilitate the global energy transition and present compelling investment opportunities.

US-250522-175517-1

- IPCC, Press release, April 4, 2022Opens in new window

- IPCC, Climate change 2022, Mitigation of climate change, Summary for policymakers, 2022.Opens in new window

- Ibid

- Ibid

- Ibid

- The Institutional Investors Group on Climate Change, Climate Investment Roadmap, 2022.Opens in new window

- Through May 5, 2022

- Bloomberg, May 5, 2022

- Ibid